By Kjeld Herreman, co-founder at Paylume.

Last month in Copenhagen, Paylume’s co-founder Kjeld Herreman moderated an expert panel at EBAday 2026 that unpacked how banks in Europe can move beyond ISO 20022 compliance to unlock richer data, real-time processing, and new services while addressing the operational challenges that migration has exposed.

The ISO 20022 migration story has largely been told as one of compliance: deadlines that need to be met, message formats that need to be updated, and gateway infrastructure that must be deployed.

And across banks and corporates alike, the focus on getting to full compliance has, in many cases, obscured the harder work that follows. Although the migration of payment instructions to the ISO 20022 format has been completed in November of 2025, most of these messages are not yet leveraging the rich data capabilities the new data format allows for.

Introducing the ISO 20022 standard was never the end goal. It was just the start of the beginning: setting a baseline communication standard that can be used for faster, cheaper, and more secure payments. And there’s still a long way to go.

When the audience was polled, about half of the audience had not yet perceived any tangible benefits from the introduction of the standard.

However, this is set to change over the coming years, with the introduction of more structured data requirements and extended message sets.

Structured addresses: the defining challenge of 2026

Structured addresses are the key ISO 20022 challenge for 2026. From November, unstructured addresses will no longer be accepted, and financial institutions will need to introduce structured or hybrid addresses to more unambiguosly identify parties. This is a huge technological uplift not only for payment service providers, but also for corporate clients, that will need to provide their banks with structured beneficiary details when initiating payments using files or APIs.

However, the panel agreed that the benefits of this uplift will outweigh the costs. Gone are the days of false positive sanctions hits when processing transactions from “Rue du Teheran” in Paris. The panel further agreed that these benefits were also realised using hybrid addresses, and emphasised that the hybrid address is not just a transitory measure, but a long-term solution that is not set to be phased out.

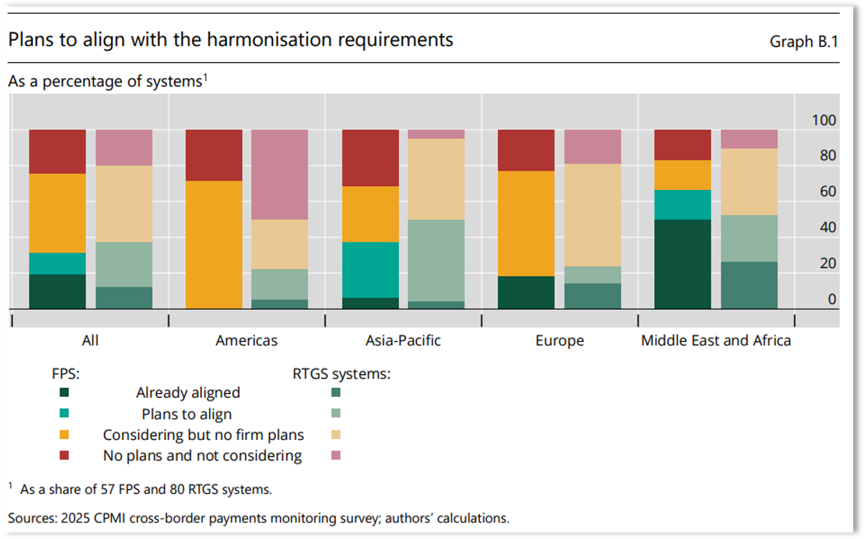

Alignment and interoperability

The Bank of International Settlments’ Committee on Payments and Market Infrstructures (CPMI) has laid out recommendations for harmonised ISO 20022 messaging to enhance cost and speed in international payments, in line with the G20 roadmap for cross-border payments. Although progress has been made to align messaging standards for RTGS and Faster Payment systems, there is still much work to do.

In Europe, work has started on aligning with the CPMI harmonisation requirements; which include annual base-message upgrades. In the latest consultation on SEPA payment schemes, we know the European Payments Council is exploring base-message uplifts as from the November 2029 release. The panel further talked about challenges in the United Kingdom, where Faster Payments is still using the ISO 8583 (card) standard.

Exceptions & investigations

Another key change the industry needs to deal with is the migration of exceptions and investigations messages to the ISO 20022 standard. Historically, payment investigations relied on unstructured, manual messaging, which led to delays, limited visibility and high operational costs.

The move to structured ISO 20022 case management messages enables greater automation, improved tracking, faster resolution times and better data quality across the payment chain.

However, firms will need to upgrade legacy systems, adapt operational processes and prepare for the phased retirement of legacy MT-based investigation messages through 2027.

ISO 20022 and instant payments

ISO 20022 is transforming instant payments by enabling richer, structured and machine-readable data to move alongside funds.

This improves straight-through processing, enhances fraud and sanctions screening, supports automated reconciliation, and enables services such as Request to Pay and real-time payment tracking.

It also improves interoperability between domestic and cross-border payment systems, helping create a more connected global payments ecosystem.

While the benefits are significant, banks must modernise legacy systems and improve data quality to fully realise them. In short, real-time payments deliver the speed, while ISO 20022 delivers the intelligence, transparency and automation that make instant payments more valuable for businesses, consumers and financial institutions.

Updated FATF Recommendation 16

This is playing out at the same time as ISO 20022 and the FATF’s revised Recommendation 16 are becoming mutually reinforcing, an issue raised by those on the panel.

FATF defines what payment information must accompany a transaction, such as originator and beneficiary details for AML, sanctions screening and fraud prevention, while ISO 20022 provides how that information is structured and exchanged.

By 2030, for transactions above the de-minimis threshold of 1000 EUR/USD/GBP, PSPs will need to include the payer’s date of birth or company identifier, and the payee’s company identifier if the payee is not a natural person. Although providing this information will be a great challenge for the industry, the benefits are clear, as the number of false positive financial crime compliance hits is set to drastically reduce thanks to this more precise way of identifying parties to a transaction.

From message format to data quality

ISO 20022 is about structured, machine-readable payment data, not XML. It requires explicit details like addresses and remittance data, exposing gaps where many organisations find true compliance more challenging.

For corporates in particular, the obstacle is not the standard itself but the condition of the underlying data. Supplier and customer records are frequently incomplete or inconsistent, spread across ERP systems, procurement platforms, and treasury tools that were never designed to maintain the structured address fields or party identifiers ISO 20022 now demands. Poor-quality source data does not disappear in transit; it surfaces as payment exceptions, manual investigations, reconciliation failures, and compliance exposure.

The November 2026 deadline for structured addresses on SWIFT traffic makes this a live problem today, not a future consideration.

It is not without its risk

The optimism that surrounds open finance on the continent must be weighed against genuine risks. Data privacy breaches become more consequential as financial data becomes more portable. Consumer harm is a realistic concern in markets where consumer protection enforcement is still developing, with some nations still drafting consumer protection regulations. Cenfri’s work emphasises that open finance implementation “typically unfolds in phases over five to seven years,” requiring regulators to resist pressure to move faster than their oversight capacity allows.

There is also the risk of exacerbating inequality. If open finance frameworks are designed primarily around smartphone-based consent interfaces, urban broadband connectivity, and formal employment records, they may deepen the financial exclusion of the populations they were meant to serve. The design choices made across the continent over the next three to five years will determine whether Africa’s open finance moment is genuinely inclusive or whether it creates a two-tier system that serves the already-served.

The phased reality of where the industry stands

ISO 20022 adoption can be viewed in phases.

Phase one focused on message migration and scheme compliance.

Phase two, now underway, centres on data quality and ISO-native processing, including structured addresses, enriched remittance data, and removing internal translation layers.

Finally, phase three, still emerging, is about monetisation through analytics, forecasting, and AI-driven services.

ISO 20022 marks a distinct shift towards more intelligent, data-driven payments. Paylume works with financial institutions to turn compliance into real advantage. We provide clear education on evolving standards and practical advice that links requirements to business priorities.

Our team helps improve data governance, address structured data challenges and make better use of enriched payment information. With hands-on support, we modernise payment messaging, streamline operations and help you prepare for the future.