Many small and medium-sized enterprises find traditional banking slow and inflexible. In this blog, Paylume’s Lauren Jones explains why open banking now offers SMEs faster, more transparent financial solutions and services.

Navigating banking as an SME can mean navigating pain points such as long delays for credit decisions, manual account reconciliation and fragmented cash-flow data.

This makes engaging with financial services a challenge.

Yet, open banking is starting to reshape SME finance by opening up secure access to bank data via APIs and enabling new, innovative services.

The number of open banking users worldwide reportedly surpassed 470 million in 2025, with a projected rise to 645 million by 2029.

Yet while millions of consumers use open banking tools, SME adoption remains uneven globally.

From London to São Paulo, Sydney to Mumbai, small businesses often face structural, operational, and psychological barriers to adoption.

Why should SMEs embrace it?

Real-time cash-flow insights: Open banking-enabled accounting platforms such as Xero and QuickBooks automatically pull bank transactions so SMEs can see balances and cash positions across multiple accounts without manual uploads, boosting forecasting and budgeting.

Faster, cheaper payments: Companies can initiate payments directly from bank accounts, bypassing cards and reducing fees, which improves cash flow and speeds up settlement.

Access to finance: By sharing financial transaction data with lenders, SMEs enable more accurate risk assessments and faster credit decisions than traditional credit-score-only models

The UK: A mature open banking ecosystem

The UK is widely seen as a global leader in open banking, with a strong regulatory regime and high adoption rates.

As of 2025, 15.16 million people and businesses in the UK are utilising open banking (up 40 % year-on-year), and this includes about 750,000 UK SMEs (roughly 16% of firms) who were actively using open banking tools, a figure that has continued to rise as products evolve beyond account aggregation to payments and lending.

There are already examples in the market of open banking supporting SMEs. GoCardless uses open banking and direct debit rails to provide frictionless payment solutions for merchants and SMEs. This enables businesses to collect invoices, subscriptions, and recurring payments directly from a customer’s bank account with lower fees than card networks.

As of 2025, it’s used by 100,000 businesses and processes $130 billion annually.

As Variable Recurring Payments (VRPs) look set to be implemented, merchants will be able automate subscription payments to automate billing while giving customers transparency and control over what and when payments are taken.

Obstacles to implementation

That being said, there are clear obstacles to widespread usage in the SME sector.

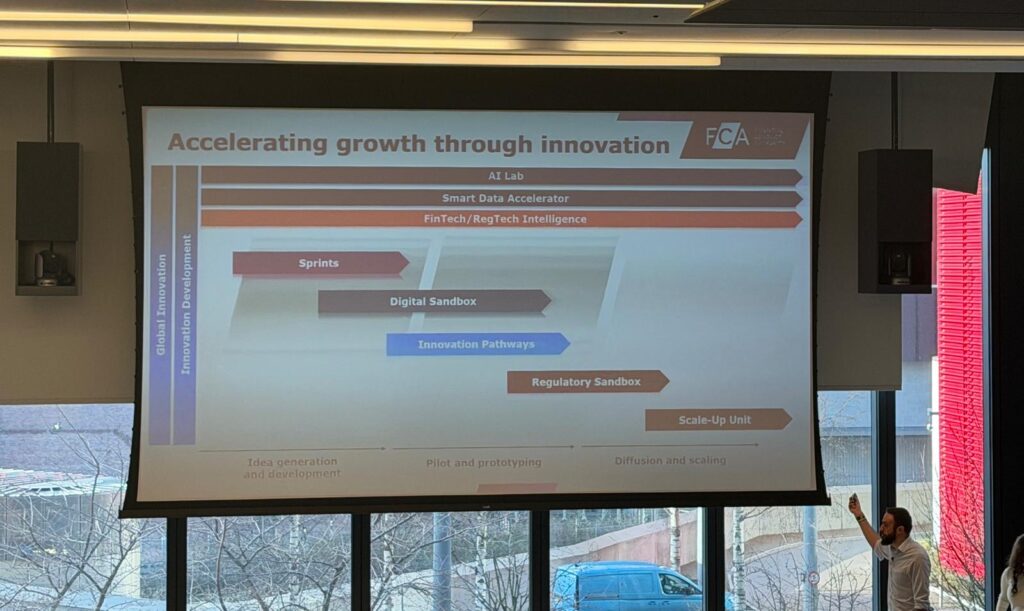

The Financial Conduct Authority recently held an Open Finance Tech Sprint focusing on SME lending as part of its Smart Data Accelerator.

It was noted that only 34% of businesses have an existing credit line, many citing too much paperwork as a challenge. While solutions are starting to blossom, banking data is only part of the solution story. Many vendors would like to see this supplemented with payroll data and credit bureau data to paint a fuller picture of a business’ creditworthiness.

The FCA are clear that experimentation delivers benefits and will lead to better policymaking, and it is using the Smart Data Accelerator to understand the challenges in SME adoption.

Enhanced lending capabilities

Open banking can better support SME lending by enabling secure, real-time sharing of financial data, resulting in faster decisions, reduced paperwork, and more tailored, accessible credit. Instead of relying on manual, outdated documents lenders use recent transaction history to assess current cash flow, improving approval rates for SMEs with thin credit histories.

Fintech credit engines like Algoan in France use open banking data to improve SME and consumer lending decisions by accessing real-time income, spending patterns and financial health indicators.

Lenders using these models have reported up to 40% more loans issued and a 50% reduction in credit risk because they can assess applicants with richer, current data instead of traditional bureau scores alone. Sofinco, a subsidiary of Crédit Agricole Personal Finance & Mobility, is a major player in consumer financing in France.

- During the credit application process, after entering a few details, customers are invited to connect one or more of their bank accounts via a secure interface.

- Algoan retrieves relevant banking data (income, expenses, incidents, etc.) via API.

- This data is then analysed to generate affordability indicators and a behavioural credit score.

- Sofinco integrates these results into its decision-making process to deliver an instant and tailored response.

Sofinco has recorded significant performance gains, including an increase of nearly 35% in GINI.

Not all ecosystems are created equal

Despite markets like Brazil being considered at the forefront of open banking, SME adoption is still low. According to a recent industry study, only about 3% of companies in Brazil are currently connected to open banking products.

However, where it is being utilised the benefits are clear. According to Agência Brasil, open banking mechanisms in Brazil have already helped increase credit approval rates by up to 30% for borrowers by sharing financial data across institutions. Conta Azul integrated open banking to let small businesses reduce credit approval times from 15 days to about 4 hours, helping them react faster to financing needs and avoid lost opportunities.

In Australia, despite having open banking for nearly as long as the UK only a very small percentage of Australian bank customers (well under 1%) have active CDR data-sharing arrangements. SME participation is even lower because business accounts were onboarded later and require more complex consent processes.

Screenscraping has also not disappeared for Australia yet. Many accounting or fintech platforms find screen scraping is cheaper and requires less regulatory overhead. As long as alternative data access methods remain available, SMEs don’t feel urgency to migrate to an API-based approach.

What are the adoption barriers?

Awareness gaps

It is true that SMEs do not need to be familiar with the terminology of open banking. However, they do need to understand about how it works and how it differs from traditional bank feeds in accounting software. Many smaller firms associate open banking only with “sharing data” rather than with tangible benefits like faster lending approvals, pay-by-bank payments or automated reconciliation

For micro-businesses without dedicated finance teams, the concept can feel abstract.

Complex consent journey and poor user experience

Open banking relies on explicit, revocable consent which is positive for data protection and privacy but can create friction. In Brazil, businesses often require multiple legal representatives to authorise data sharing and re-authentication requirements can disrupt workflows.

This has slowed SME take-up compared to consumer usage.

Integration costs

Open banking is API-driven but integration isn’t always plug-and-play. SMEs may face additional software or licensing upgrade costs.

In Australia, some smaller banks and fintechs have raised concerns about open banking compliance costs. If providers pass these costs on to end users, SME adoption will be slow. For small firms, even minor IT friction can stall adoption.

Security concerns

Security perception is one of the biggest global barriers. Even where regulation is robust, SMEs may worry who can see their data and if it is less safe than logging into online banking. Some SMEs still prefer manual bank transfers over pay-by-bank because they “trust what they know.” For some, the perceived risk often outweighs efficiency gains.

Limited immediate ROI for some SMEs

For many SMEs, a spreadsheet can feel sufficient to undertake their accounting and cash visibility tasks and manual bank transfers can feel manageable, and for some, their lending needs are occasional and not continuous therefore adoption can feel unnecessary.

Bank readiness

In some countries not all banks provide equally stable APIs and in particular smaller institutions may lag behind or not be in scope of regulation (UK).

In Australia, the phased rollout meant uneven early experiences and in India some financial institutions joined the Account Aggregation framework gradually.

While in the UK, there is still only a mandate for the largest nine retail banks to share data.

This inconsistent data quality reduces SME confidence.

The move forward

Open banking is technologically ready, but SME adoption is about so much more.

Education. Trust. Simplicity. Clear economic incentives.

As open banking ecosystems mature the key shift will likely come from embedding open banking invisibly inside everyday SME tools. When it becomes invisible infrastructure rather than a decision adoption will accelerate.

If you need support in developing your SME open banking proposition, get in touch today at [email protected].